TL;DR:Financial services marketers face stricter advertising, privacy, and disclosure rules from regulators like FINRA and the SEC, along with added state and global oversight. That means tighter controls around claims, consent, data use, and approvals across every channel. Centralizing processes, standardizing disclosures, and using helpful tools to manage permissions and audit trails can help teams reduce risk, stay compliant, and scale campaigns with confidence.

Intoduction

The Financial Industry Regulatory Authority, the Securities and Exchange Commission, local regulations, and privacy laws … it’s a lot to contend with, isn’t it? You likely already have enough on your plate, working to prove your marketing’s impact to leadership and helping your team feel less overloaded. But at the same time, you know that when it comes to compliance, you can’t afford any mistakes.

Whether you’re brushing up on financial services advertising regulations for 2026 or you’re new to the industry and figuring out which ones to watch, we’ve broken down the most important ones, along with tips for keeping up at scale when your team is already stretched too thin.

Why Advertising Regulations Matter More for Financial Services

As a financial services marketer, you likely have a long list of goals to hit this year. The challenge is reaching those goals while checking all the important compliance boxes. And this year, advertising regulations matter even more because:

Consumer trust is key

The trust required for financial transactions is significant. People don’t casually try out a new bank the way they might stop by a new restaurant for takeout on the way home from work. And that sets the bar for credibility even higher.

Plus, the stakes are serious. More than half of respondents have considered switching financial institutions in the past two years. So, you don’t want to break trust for any reason, especially not when it comes to financial services advertising regulations.

Regulatory security continues to tighten

Stricter rules on consumer data collection from the Federal Trade Commission, along with increased oversight of advertising claims and disclosures from the Securities and Exchange Commission and the Financial Industry Regulatory Authority, make it harder for financial marketers to stay compliant and do so at scale.

Risk of noncompliance comes at a great cost

Strict regulations also bring the risk of fines, not to mention the potential for broken trust and reputational damage. As the number of marketing channels has grown over the years, financial marketers now face compliance risks from many directions.

For example, a bank was recently fined $850,000 by the Financial Industry Regulatory Authority for sharing social media posts from an influencer that weren’t considered fair or balanced and included exaggerated, unwarranted, promissory, or misleading claims.

Key Financial Services Advertising Regulations to Know in 2026

As a financial marketer, it’s your job to understand which regulations you need to follow and how to stay compliant across all the channels you manage. But which ones matter most? Here are a few financial services advertising regulations to watch in 2026, including:

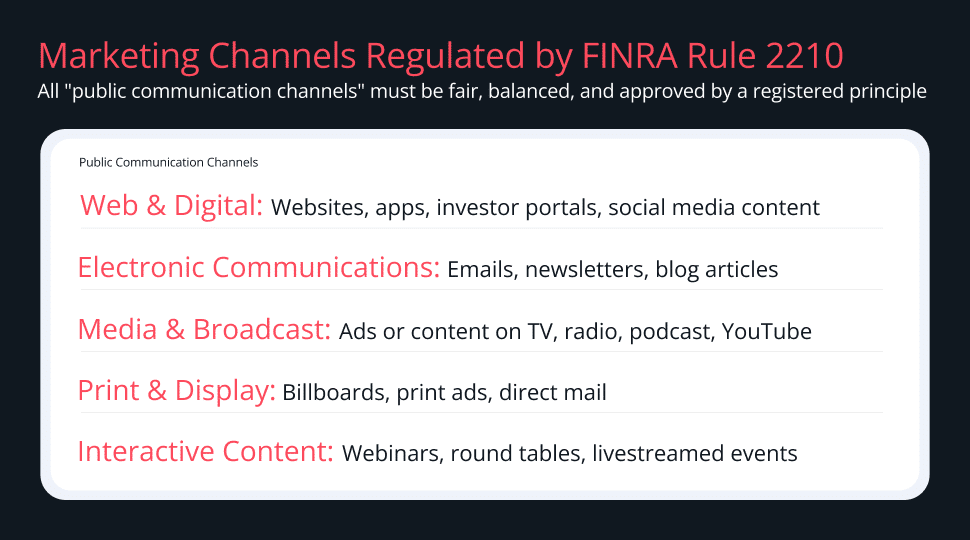

1. FINRA Advertising and Communications Rules

FINRA compliance focuses on standards that require your communications with the people you serve to be fair and balanced and not misleading. It covers things like the emails you send, the content on your website, your social media posts, and the brochures your team puts out into the world.

FINRA Rule 2210 is the main rule that governs how you communicate with the public through marketing, advertising, and promotional content. These regulations set expectations around disclosures, substantiated claims, and supervisory oversight across channels.

2. SEC Marketing and Disclosure Requirements

The U.S. Securities and Exchange Commission oversees investment adviser marketing standards under the Investment Advisers Act of 1940, and its modernized marketing rule clarifies exactly how advisers must present performance data, testimonials, endorsements, and third-party ratings in their promotional content.

For example, regulators recently held nine firms accountable for violating the marketing rule. They were called to account for “disseminating advertising that included untrue or unsubstantiated statements of material fact or testimonials, endorsements or third-party ratings that lacked the required disclosures.” The organizations ended up paying roughly $1.2 million in combined civil penalties.

3. State-Level and Global Oversight Considerations

Beyond federal rules, you’ll also need to account for state regulations and global oversight. U.S. states enforce their own consumer protection laws, which often prohibit unfair or deceptive practices and can be used to challenge misleading marketing. If you operate across borders, international requirements also apply. For example, the Financial Conduct Authority in the UK has specific rules governing financial promotions.

So, you’ll want to track not only the advertising regulations for financial services and federal laws but also any regulations that apply to the specific geographies where your organization operates.

Financial Services Data Privacy Regulations and Marketing

With technology advancing quickly and more tools collecting and using data for all types of purposes, consumers are understandably concerned. They want to know who has their data and how it’s being used. And the laws are working to catch up. Here are a few areas to watch around financial services data privacy regulations:

Data collection and consent

Before you start collecting data, make sure you collect it lawfully and clearly document your process. Your customers and the people you serve need to actively consent to specific uses of their information. Examples of privacy laws include the California Consumer Privacy Act (CCPA) and broader regulations like the European Union’s General Data Protection Regulation (GDPR).

Privacy requirements also mean you’ll want to build consent capture into your forms, landing pages, and anywhere else you gather data. Standardize the language and carefully track the purpose and use of each data type. You’ll also want an efficient way to store those records so you can demonstrate compliance, whether you’re using the data for email marketing, segmentation, or something else.

Storage use and considerations

Data privacy in financial services doesn’t only govern what types of data you collect. The regulations also govern how you store and safeguard that data. That means protecting customer data from unauthorized access and using it only for the purposes to which people consent. In practice, this often includes strong access controls, encrypted storage, and clear retention and secure disposal policies.

For marketing teams, that means being intentional about where customer lists and behavioral data live. Disconnected spreadsheets and ad hoc processes can create security and compliance issues, especially when you need audit trails, documentation, and clear oversight.

Impact on targeting and personalization

Financial services data privacy rules often change how you approach segmentation and personalization. When broad consent isn’t possible, you may need to rely more on context-based targeting or aggregated data instead. Rather than using detailed individual profiles to trigger a nurture email, you might structure journeys around life cycle stages or high-level behaviors that don’t require sensitive personal information.

Regulations like the California Consumer Privacy Act and the General Data Protection Regulation make it harder to depend on highly granular personal data without clear permission, which naturally shifts teams toward broader privacy-safe approaches.

Cross-channel personalization can also get more complicated, especially when it involves third-party cookies or external data sharing. Those tactics need careful review against current privacy requirements. Focusing on strong first-party data practices, like opt-in lists, owned analytics, and clear audit trails, helps you execute effective marketing while reducing the risk of crossing regulatory lines.

How Advertising Regulations Affect Different Marketing Channels

Regulations don’t only impact what you can say but also the operations of your different marketing channels. Every channel needs to be easy to review and to show compliance. A few examples include:

Email marketing and compliance

When crafting email marketing strategies for financial services, you’re often entering regulated territory. Some tools allow you to create templates that lock in those disclosures so your team can’t edit or remove them without the proper permissions.

Digital advertising and content marketing

Paid ads, landing pages, blogs, and social posts are all examples of content that might fall under financial services advertising regulations. But the challenge is often related to the overall scale. For example, you might have dozens of ad variants to manage. Teams can centralize approved claims and disclosures, then build campaigns using that approved content. This speeds up creation and helps reduce risk.

Campaign approvals and recordkeeping

Every new campaign goes through legal review and approval, and you need to document that it happened. Tracking approvals and related communications in one system helps you move faster without missing important oversight steps.

How Marketing Automation Helps Financial Services Stay Compliant

As you build broader marketing strategies for financial services, compliance becomes trickier at scale. The more segments and campaigns you’re running, the higher the chance that something gets overlooked. Manual processes can create additional issues, but marketing automation software can help address them with the following:

Centralized control

When campaigns live across multiple tools and technologies, it’s easy for outdated copy or unapproved claims to slip through. Marketing automation helps you centralize templates and create fixed blocks so all the important compliance pieces stay intact.

For example, teams can lock required risk language into email and landing page templates so it can’t be changed accidentally. Marketers can then build from those approved components rather than starting from scratch with every campaign.

Permission management

Privacy regulations and internal policies often require clear direction about who can contact which customers. Consent, opt-out, and channel preferences all need to be followed, and manual tracking can be risky.

Marketing automation helps fix this by ensuring each contact record and its preferences are enforced. If a customer decides to opt out of a channel, they’re automatically excluded from future sends.

Audit trails and consistency

Regulators often expect proof. You need to show what was sent, when it went out, who received it, and which version of the content was approved.

Built-in audit trails make that possible. Archived messages, version histories, and documented approvals help you run compliant campaigns and confidently defend them during audits.

Preparing Your Marketing Team for 2026 and Beyond

Compliance might be a large part of your job, but that doesn’t mean it has to weigh heavily on your team. With the right tools and resources, you can still creatively reach your audience with the content they need at the right time while staying compliant with financial services advertising regulations.

Purpose built tools like Act-On’s marketing automation for financial services help you strike the balance between executing what’s needed to reach your goals and not accidentally stepping into costly compliance violations.