TL;DR: With the great wealth transfer underway and customer expectations rising, retail banks have an opportunity to strengthen relationships and drive growth. Aligning with key retail bank marketing trends, like using first-party data to personalize outreach, connecting engagement across channels, building thoughtful lifecycle programs, and leaning into automation to scale execution, teams can show up at the right moment and with the right message.

Introduction

Growth is an important part of most marketing strategies. And if you’re like many retail bank marketing teams, it’s high up on the list, especially growing deposits in the current environment. In fact, McKinsey & Company describes deposits as a “top profitability lever for retail banks.”

But how do you reach more prospective customers and retain your existing ones, regardless of what you’d like to promote? We’ve found one of the easiest ways to build momentum is to piggyback on current trends. Because when you understand which retail bank marketing trends are in motion, you can execute strategies that align with them and capture an advantage in the coming months.

Why Retail Bank Marketing is Changing

Most retail banking customers don’t start their journey with a conversation at a local branch. They start with a search bar. They compare loan rates on their phone during lunch, check reviews at night, and open new accounts while sitting on their couch. In fact, 77% of banking customers say they prefer to manage their interactions through a mobile app or computer.

Add to that the fact that the prospects most likely to prefer digital banking experiences are millennials (80%), who are set to receive the largest share of the Great Wealth Transfer, as they are expected to inherit roughly $46 trillion through 2048.

And while being present on digital channels certainly isn’t new, expectations around those experiences are changing. Retail banking customers expect an incredibly high level of personalization. It goes far beyond “Hello, Name.” They want marketing that’s relevant to their needs in the moment, like a first-time homebuyer who checks rates on your site and then receives a timely email about down payment assistance programs.

At the same time, fintechs are nipping at your heels and working hard to redefine what “good” looks like. They launch quickly and run highly targeted email campaigns to win niche segments, such as high-yield savings or peer-to-peer payments.

As a result, your retail bank isn’t competing only on rates but also on speed, personalization, and convenience.

Five Retail Bank Marketing Trends to Watch in 2026

As you work to capture the interest of customers and prospects, one of the easiest ways to drive success is to build on 2026 bank marketing trends already in motion. Here are five to watch this year:

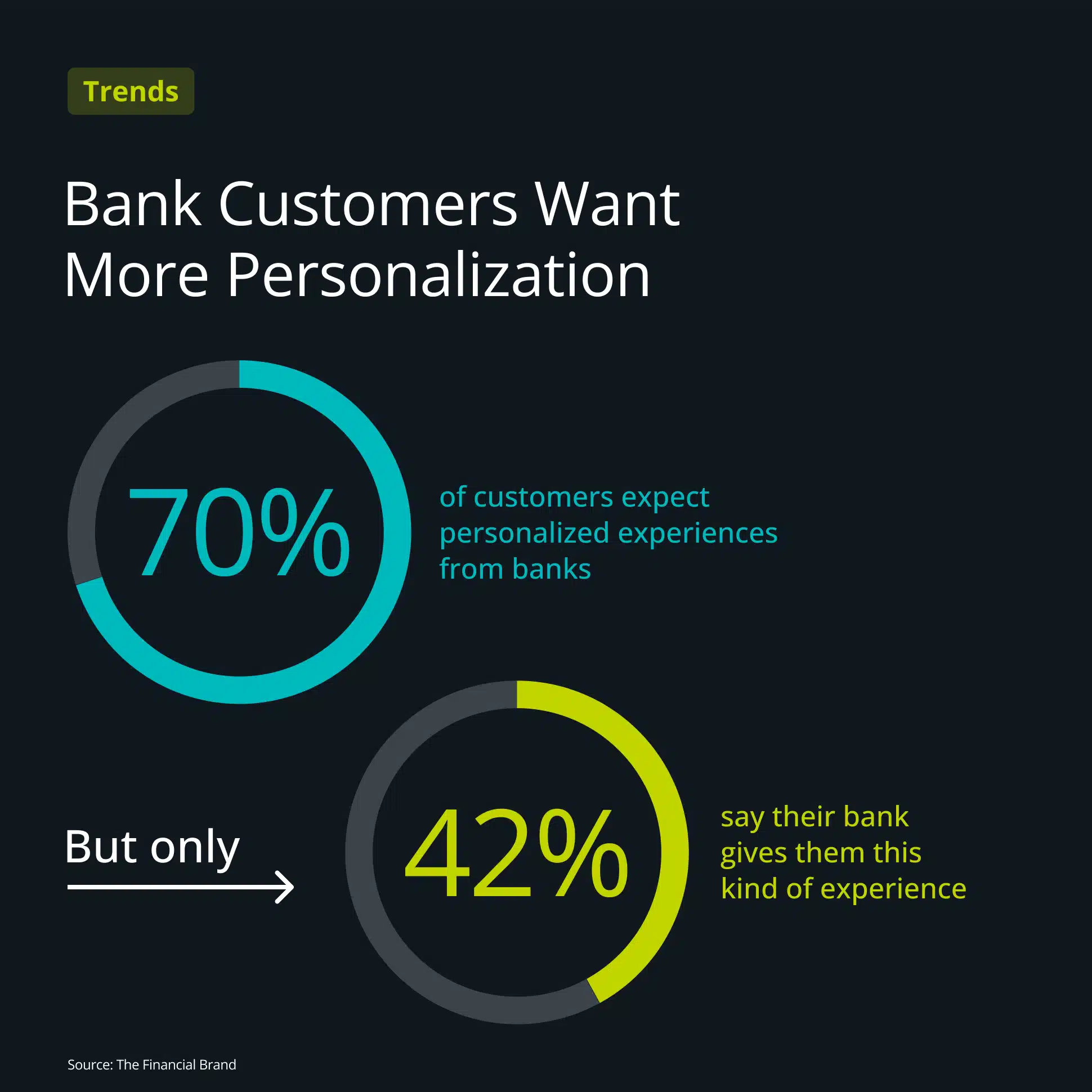

1. Personalization Becomes Mandatory in Banking

Most consumers, roughly 70%, want personalized banking advice, but only 42% say they actually receive it, which creates a huge opportunity for retail bank marketing. At the same time, customers don’t want to feel like you’ve sliced and diced them into segments and blasted out semi-personalized emails.

So if you’re going to catch a tailwind with this trend, you need the right data. If you can understand what actions customers are taking in the moment, you can show up with solutions and resources that help solve their challenges. It’s a little like mind reading, but on a much larger, data-backed scale.

2. First-Party Data and Trust Drive Marketing Strategy

There’s definitely a place for third-party data with retail bank marketing, but what often goes underutilized is the data you already own: your first-party data.

With first-party data, you can tap into valuable information about your existing customers, such as account activity, product holdings, digital behavior, and interactions both online and in your branches. Those insights can help you understand what people need and when they need it, so you don’t miss the moment. You can also segment more effectively and reduce off-target outreach, such as pitching a first-time homebuyer a new business loan.

And with more relevant messages, your customers will start to trust you more, and conversions will tick upward.

3. Omnichannel Engagement Replaces Single-Channel Campaigns

Your customers bounce between their inbox, mobile devices, social media, and your website. So you might create an amazing campaign on one channel, but if you don’t connect behavior across all of them, you miss incredibly helpful context.

A prospective customer might browse rates on your site, start an application, and then abandon it because it takes too long. Later that week, they might stop by a branch for an unrelated issue, and the staff have no idea they’re in the market for a loan. If they did, they could start a conversation and help guide them through the process. When you understand and leverage omnichannel marketing, conversations increase, and customers feel more known, building trust.

And the reality is that customers want a better experience. One survey found that when asked about frustrations with their bank, eight out of 10 pointed to disjointed experiences between channels and nearly two-thirds said difficulty accessing information was a problem. And that means there’s a ton of opportunity here.

4. Lifecycle Marketing Takes Priority Over One-Off Promotions

One-time promotions can create short spikes in activity, but they don’t always build long-term value. Lifecycle marketing programs take a different approach. They focus on the key moments that matter most to your customers, like onboarding, the first deposit, cross-selling, and retention. For example, you might create a structured onboarding series that guides customers through important actions, such as paying bills online, making mobile deposits, and using peer-to-peer payments.

Sure, you might still run a few one-time promotions, but lifecycle marketing is becoming more important as retail banks brace for the great wealth transfer, helping you win new business and retain the customers you already have. These programs make customers feel supported, so they’re more likely to stay and do more with you. That also makes performance more predictable and easier to manage.

5. Marketing Technology and Automation Gain Strategic Importance

As the need for personalization grows and data usage spans multiple channels, manual execution can falter, especially with a smaller team.

Retail bank marketing teams benefit from systems that help standardize processes, trigger communications based on your customers’ behavior, and view performance across the entire funnel. For example, a marketing automation platform can route leads based on product interest and send follow-ups after key actions are taken, like starting an application, so outreach feels more relevant without requiring a ton of manual effort.

It also creates consistency, and that’s often the hard part when your retail bank marketing team is super busy, right? It lets you deliver the right message at the right time to thousands without adding head count to your team.

What These Retail Bank Marketing Trends Mean for You

Change isn’t always a bad thing, and oftentimes, especially with these trends, it can actually be good. When you can optimize your bank marketing strategy with trends like digging into personalization with first-party data and showing up where and when customers need you, you can capture opportunities that weren’t possible in the past.

The caveat is that data discipline becomes an even bigger priority. What you don’t want is customer data scattered across your systems, online banking platform, and CRM, which makes it hard to shape into something marketing can actually use. You need a clear view of who each customer is, what products they have, and how they behave across different channels. With this type of insight, your team can prioritize high-value segments and route budget to where it makes the biggest impact.

And as you shift from one-off campaigns to a more coordinated journey built on strong data, instead of asking, “What are we promoting this quarter?” you can start asking questions like, “What should a customer’s first 90 days with us look like?” or “How do we identify and engage customers who are most likely to refinance?” This shift helps you create repeatable programs that run continuously and drive long-term results.

Preparing Your Retail Bank for What’s Next

As you move into the months ahead, you likely have a lot of goals, and some of them might feel difficult to reach. Sometimes the constraints come down to execution. When you have tools that support you, you can execute at a scale that wasn’t possible before, reach more of the people you serve at the right time, and deliver results that are repeatable and help you prove marketing’s value to leadership.

If you’d like to explore more about how marketing automation for banks can help your retail bank marketing team, we can help.